While more than 70 percent of Americans believe that they have good financial knowledge, FINRA found that only 40% of them could correctly answer 4 out of 6 basic financial questions. The same is the case for most working-class Americans, who didn't have access to any financial education. They have been renting houses and spending money and have yet to learn about the financial tricks of saving, investing, and creating wealth.

Financial literacy month is celebrated every April. This month is dedicated to raising awareness about financial literacy and promoting financial education. Individuals have an opportunity to reflect upon their financial situation during this time and to learn more about how they can better manage their finances.

It doesn't matter whether you're earning six figures or doing odd jobs to make your living. Being aware of your financial well-being is equally crucial for all of us. If you need a grasp of finances, you are not alone.

This article intends to answer some important finance queries to help you make yourself financially resilient and literate.

What is Financial Literacy?

Despite its growing popularity, there's yet to be a single, agreed-upon definition of financial literacy. It is a concept that emphasizes having considerable financial skills like budgeting, saving, and investing that help you make smart financial decisions.

To be financially literate means, you are aware of managing your money better. It means learning how to pay your bills and meet your expenditures while saving for your retirement. Financial literacy backs up the concept of self-sufficiency and promotes economic resilience for individuals. It comprises four key components: knowledge, skills, attitudes, and behavior.

Implementing knowledge for financial literacy includes having an adept understanding of key financial concepts like inflation and compound interest. It also provides awareness about financial wellness products and services, as well as practical skills about making payments and saving for the future.

Why is it important?

Financial responsibilities are on the rise for an individual today. They play an essential role in every facet of life. Thus, being financially literate is the only way to make wise financial decisions.

Financial literacy paves the way for individuals to plan for their life ahead and have instant emergency funds. It helps create responsible citizens who value the significance of spending wisely with the right amount of wealth spent to help others. It also helps to reduce mental stress, impacting your overall health, relationships, and quality of life.

Read more about: Why is Financial Wellness Important?

Addressing the Big Financial Questions

Wherever you are on the journey to financial wellness, there are always more questions: How to best handle student loan debt? How to finance a home? How to fund my child’s college education? But regardless of any factor or degree of financial literacy, three big questions are commonly asked by individuals on their way to becoming more financially fit.

With each question, remember that the financial goal itself is not the only achievement. Each goal is also a step toward achieving financial wellness, intelligence, and independence. Let’s break down these three big financial questions and their popular answers.

#1: How do I improve my credit score?

This is a challenge that most Americans face, no matter where they are on the path to financial health. Improving your credit can take time, but making that effort now will set you up for significantly lower costs on mortgages, loans, and even insurance. Depending on your individual circumstance and financial bandwidth, the specific answer will vary on the best ways to improve a credit score. Still, there are basic principles that apply in every case.

Here are the five keys to increasing your credit score:

- Make timely payments for all accounts

- Avoid loans as much as you can

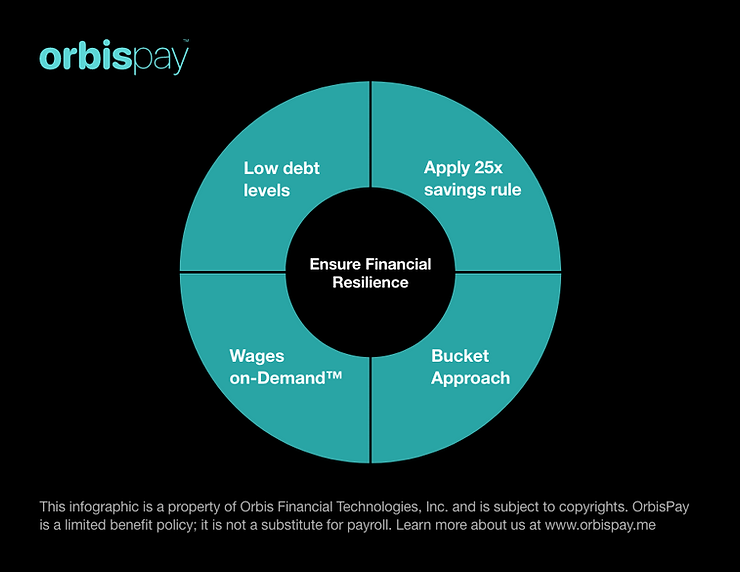

- Keep your overall debt levels low

- Monitor your credit report for errors and omissions

- Avoid opening accounts that you don’t need and keep accounts that lengthen your credit history

Another popular solution to improving a credit score when there is little to no credit history, is to seek the aid of non-traditional credit score options. Credit scores are an efficient way for lenders to identify the likelihood of a borrower repaying their loan request based on the repayment of past loans. Though this may be an efficient process, it doesn't consider the financially responsible individuals who have never requested a loan.

Non-traditional credit score options will help to establish credit for these individuals based on accounts that incur regular payments, such as rent, utility payments, or cell phone payments. If you’re a recent immigrant or a young adult with no credit history, this may be a perfect option to build positive credit quickly based on your good financial habits.

#2: How do I save for retirement?

It may seem like a question that is easy to put off, especially for younger adults who feel that retirement is decades away and worlds apart, so there’s plenty of time to think about it later. However, a bit of financial literacy will convince you; the sooner you take action on a retirement plan, the better off you’ll be as the decades fly by and that world gets closer.

People want to know when to begin saving for retirement, how much money they should contribute regularly, and how often. Saving for retirement, or even an emergency fund, can be approached using the popular 25x rule.

The 25x savings rule sets a baseline retirement savings amount for you. To calculate this amount, take your current total of monthly expenses (be thorough) and multiply that by 12 months for an average annual expense amount. Take that annual expense and multiply it by 25. This is the amount to aim for in your retirement savings account.

Let’s say your monthly expenses are $2,500, so annually, that’s $30,000. Now we multiply $30,000 x 25 for a total of $750,000. Though a number like that may sound challenging or unattainable, it’s certainly possible to accomplish by starting as early as you can, regularly contributing a reasonable percentage of wages to this goal, and making yourself aware of employer matching perks, supplemental income, and other ways to meet this goal faster.

#3: How do I finance a big purchase?

A big financial purchase typically refers to an expensive purchase ($1,000 or more) that is not part of your typical monthly expenses; one that would disrupt your budget if you have not planned for it. This might be the purchase of a home appliance like a refrigerator or stove, maybe an upgrade in electronics, or maybe a trip to a tropical island.

One of the most popular ways to save for these larger expenses is by bucketing your money. This method is so named because it’s like dropping a small percentage of your wages into a bucket, or series of buckets, on a regular basis to save for the purchase. In many cases, an existing savings account is set up and earmarked for such expenses as a savings account for pet emergencies, vacations, and home repairs.

Each time you’re paid, drop some into each bucket, and in time you will accumulate enough to afford the expense. Many banking apps provide features and functionality to set up bucket savings easily and even have portions of pay funneled automatically to those accounts if you prefer.

Where Can I Find Resources for Financial Literacy?

Another commonly asked question by those seeking financial resilience is where to find the resources that teach financial literacy and promote financial wellness. This question is especially critical.

Schools and educational institutes don’t historically offer classes in financial literacy. Whether or not such a course would be added to the curriculum would be decided upon at a state level, but even so, most districts cannot find teachers who are also qualified financial advisors to conduct the lessons.

With educational institutes falling short of financial literacy, motivated individuals turn their focus to the internet for help. As you do, remember that not all sites are truly geared toward helping you. When it comes to something as sensitive as financial information, be sure to utilize trusted, verified sources.

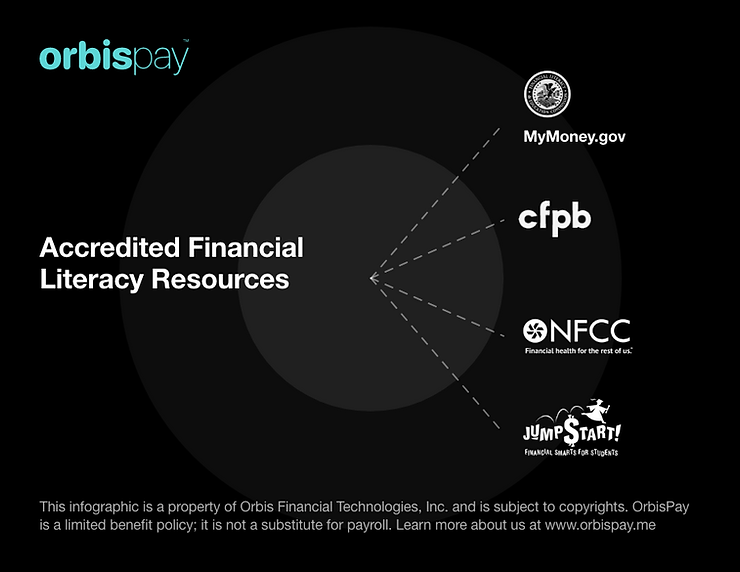

Here are a few credible and education-rich government and non-profit organizations to guide you on the path to financial wellness:

Mymoney.gov is an official website of the United States government produced by the Congressionally chartered Federal Financial Literacy and Education Commission (FLEC). Their mission is to strengthen financial capability and increase access to financial services for all Americans. This site provides valuable information about a variety of finance topics, and shares tools, worksheets, and checklists to help you achieve your financial goals.

Consumer Financial Protection Bureau (CFPB) is another U.S. government agency that focuses on the financial protection of U.S. citizens. This organization is dedicated to making the market and its products financially safe for consumers by promoting transparency and preventing abusive and deceptive practices.

https://www.consumerfinance.gov/ In addition to these resources, the following books are some of the greatest to improve your financial wisdom and provide the greatest financial insights for you:

- 'I Will Teach You To Be Rich,' by Ramit Sethi

- 'The Automatic Millionaire,' by David Bach

- 'Spend Well, Live Rich: How to Get What You Want with the Money You Have,' by Michelle Singletary

Financial Wisdom - Summed Up!

As savvy financial consumers go, we aren’t as smart as we think. In terms of financial literacy, there is always more to be learned; it’s a lifelong personal interest to seek ever-better financial wellness. We must keep our fingers on the pulse, enhancing our knowledge little by little, day by day. As our financial literacy increases, so do the rewards. Better credit, healthy savings, and access to lower rates and better deals all make it worthwhile to invest a bit of time and effort in understanding how to build financial health and resilience.

Set some time on your calendar. Sit and engage with trusted sites, institutes, and professionals for answers and guidance where you need it. Search your local community for onsite or online webinars, workshops, and courses that promote financial wellness and offer insights and education regarding financial literacy. Don’t waste another minute or dime living in confusion. Kick off Spring 2022 with a goal to nurture your financial literacy for the rest of the year, starting this April, National Financial Literacy Month.